Financial Freedom Step 2- Debt

You deserve a high five! You have not only decided to take action, but you actually have made tangible progress. A stunning number of people never make it as far as you already have.

I want to make sure you know how well you have done. I know that the result of your work from step one might not make you feel like you are in a good place, but I promise that no matter where you are now, you are in a better place than you were. I also promise that I am going to show you how to get to a better place than you are now.

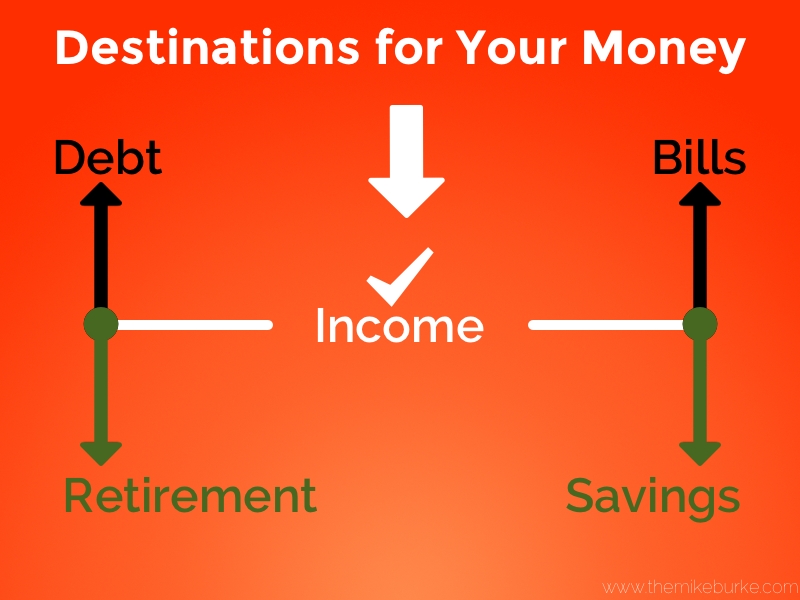

What can your money do?

The image below gives you the basic overview of the four destinations your money has. The rest of this post is dedicated to the upper left corner, debts. Look for future posts going over all the destinations.

Debt Assessment

I like to start by looking at debt because it is usually the thing that people ignore or let build in the background, but is never actually out of your mind. Not having a plan for your debt can subconsciously drain your motivation, productivity, and happiness. While you are relatively fresh and motivated, I want to tackle debt.

If you are not fresh and motivated, you should go for a walk or look at funny cat videos… anything to get pepped up. Here we go!

How to Tackle Debt

There are two schools of thought for paying off debt.

- School of Thought One: Pay off debt in order of highest interest rate to lowest interest rate.

- This is the mathematically logical, strategic choice. If you have the time, can delay gratification, and don’t need to free up money in your monthly budget, then this is the best choice. Consider this the Vulcan method.

- School of Thought Two: Pay off debt in order of the lowest balance to highest balance.

- This is commonly known as the Snowball Method; it was made famous by David Ramsey. This is the motivational and tactical choice. By picking the low hanging fruit of your debt, you get tangible wins early. You can affect immediate change and make available additional funds per month. It is key, though, that these newly available funds be used exclusively to pay down the next debt in line.

Either way, you pay the minimum amount due on all accounts and expenses except your target account. Then direct all possible funds toward your chosen debt. It’s the only way to actually beat debt!

Selecting Your Target

Now that we know how to beat debt, we have to decide which debt to beat first! Log into Mint if you haven’t done so and navigate to your debt section. Everyone’s situation is different so apply this debt hierarchy to your situation:

- Credit card debt

- Personal loans

- Student loans

- Auto loans

- Mortgage

My main criteria for the list above is interest. I have a love/hate relationship with interest, I love when companies owe me interest, but I HATE when I owe it. I found a terrifying video to help explain why interest, and particularly interest charged to credit card debt, is so bad.

Credit Card Debt

The average household has about $15,000 in credit card debt, which is less than the average student loan debt (~$32,000) and the average mortgage debt (~$154,000). So why is credit card debt my number one target? INTEREST!

As of right now, credit cards have an average interest rate of ~14%. This is sucking the life out of your financial world! Since most families have more than 1 credit card, most people have multiple interest sucking parasites to take care of. These parasites have got to go, and they have to go now!

Use one of the attack plans above to plan out how you are going to take care of credit card debt once and for all! Make sure that you do not immediately close your credit cards once you pay them off. If you think you will be too tempted to use your credit cards and get back into debt, then cancel them. But it is important to keep in mind that having a credit line open (but current and with no balance) is good for your credit score.

Power Tips (use only if you are comfortable and have done the proper homework)

- Use Mint.com to find a better credit card. Transfer your current debt to the new card with lower interest. Preferably one with a free balance transfer. Keep paying the same amount as before on the new lower interest card so that you pay down your debt faster. Remember we HATE paying interest, so we need to make decisions that reduce our interest payments.

- Consolidate your credit card debt with a personal loan. Make sure your personal loan has a fixed rate that is better than your credit card rate, has no early repayment penalty, and is with a reputable source.

Personal Loans

Personal loans are less common than the other forms of debt on our list but are certainly worth talking about. They are typically used as debt consolidation tools for credit cards. No matter how you got your personal loan, we want to get rid of it. It probably has an interest rate of about 10%, so it has got to go! Buckle down and chip away at this debt ASAP.

Power Tips (use only if you are comfortable and have done the proper homework)

- IF you are 100% responsible and aware, and you have owned your home for a while, you MIGHT find a HELOC (Home Equity Line of Credit) to be a viable option for debt consolidation. There is big danger here!If you are not committed to paying down your debt and instead use your HELOC to keep living outside of your means, not only is your debt bigger but now your home is in danger. A large part of the housing bubble of the late 2000s was connected to misuse of HELOCs. Keep in mind that a HELOC does not pay your debt. It moves your higher interest unsecured debt to a lower interest secured debt.

Student Loans

It’s hard to feel good about student loans, but hopefully the video above entertained you. This step is where that video hits a little too close to home for me, but I feel better about it because I have started taking action! The nice thing about student loans is that you can, at least, deduct some of your payment from your taxes so make sure you take advantage of that.

Depending on where you got your student loans from, the interest rate here is somewhere around 5%, so you should not look to consolidate this debt unless your student loan rate is very high. Be careful of how you consolidate this debt, if you turn it into a personal loan you may not be eligible to deduct the interest on your taxes.

Auto Loans

My wife and I just had our first child in April, so my debt strategy has actually jumped here before I finish paying off my student loans. I finished one of the three groups of student loans and decided that we would be better served to open up some more monthly cash flow. So I decided to shift to paying off my lower interest auto loan so I could open up some breathing room. I am then going to use that extra cash to help pay off the student loan debt. The benefit to this strategy is that my month to month obligation is lower. I will tell myself that I am going to pay X amount extra on my student loan, but if money is tight one month, I don’t HAVE to pay.

Hopefully, you did your best to get a good interest rate on your auto loan, so you won’t save a ton of money in interest here. But by paying off this major asset, you get increased security and open up some cash flow.

An auto loan is the first example on this list of a secured debt. That means that if I default on my car loan for long enough, someone will come to my house and take it back. The other example of a secured loan on this list is… you guessed it, your mortgage.

Mortgage

I have mortgage on here last because, while it is a debt that you want to pay off, it is the classic example of “good debt.” Your car also fits into this category but depreciates in value over time, so it is not as good of an investment as real estate. A mortgage arguably creates value in your life and eventually results in a tangible asset. Your primary residence is almost undoubtedly the single biggest investment you will ever make, so I don’t see it as a burden that must be removed like credit card debt or student loans. That being said, you should make sure that your rate is advantageous. The market is recovering so it may already be too late to refinance, but it is something you should consider.

If your other debt is all taken care of (CONGRATS!) and all you have is your mortgage, then you have two options.

- Option A: Keep it up! Pay down your last debt and enjoy a feeling of freedom that I can only imagine! It is easier than you think. You will not have to make your entire monthly payment twice. You can pay as little as $100 extra, directed at your principal, and end up saving hundreds of thousands in interest over the course of the loan. Clearly, this is 100% in line with our strategy thus far and my current plan when I get to this stage. Use the calculator found here to see how much you can save.

- Option B: It can be argued that paying off your mortgage is essentially an investment that earns you an interest rate equal to your mortgage’s APR (currently ~5%). There is a school of thought that would say that you could invest your money in the stock market and earn a higher interest rate. This would be another example of the Vulcan method. Technically it could be the better choice in the long run. I would say that having the financial security of option A would outweigh the potential upside of investing.

Next Steps

From our first post, we have a complete view of your financial landscape (debts, assets, bills, etc.) thanks to Mint. From this post, you should have a pretty good action plan for your debt. It might end up being a multi-year plan, but you can get started now. It seems impossible, but by taking action today, you can end up saving a staggering amount of money in the long run.

In the next post, we are going to get you some more great tools. I am going to show you the exact bank accounts that I use (and why). Then I will show you the (mostly) automated cash flow system that I use to manage my money.

Take a break ‘cause you deserve it!

“First comes thought; then organization of that thought, into ideas and plans; then transformation of those plans into reality.”

Napoleon Hill

Sources

http://www.nerdwallet.com/blog/credit-card-data/average-credit-card-debt-household/

http://www.bankrate.com/finance/credit-cards/rate-roundup.aspx

http://www.foxbusiness.com/personal-finance/2012/03/07/personal-loans-on-rise-but-are-right-for/

https://www.mint.com/blog/goals/how-to-use-mints-goals-06302010/

Trackbacks & Pingbacks

[…] This is part 3 on the path to Financial Freedom Series. The post assumes that you have read steps 1 and 2. […]

Leave a Reply

Want to join the discussion?Feel free to contribute!